By Case Eichenberger, Chief Investment Officer, RetirePath Advisors Published: February 2026

Global equity markets launched 2026 with conviction, posting solid gains across every major equity asset class in January. This performance builds on a trend that has gained momentum over the past six to nine months: a healthy broadening of market leadership away from the narrow concentration in mega-cap U.S. technology stocks that dominated the past several years. For clients at RetirePath Advisors, who are invested in diverse portfolios* spanning U.S. large caps, mid- and small-caps, international equities, and fixed income, this development is particularly encouraging and validates our long-standing emphasis on global allocation and balance.

January Performance Highlights

- S&P 500: +1.5% in January (trailing 12-month return: ~+16%)

- Mid- and Small-Cap Stocks: Approximately +5% in January (trailing 12-month return: ~+13.5%)

- International Stocks: Approximately +6% in January (trailing 12-month return: ~+35%)

- Bonds: Delivered strong trailing 12-month returns of around 7%, providing reliable income and a buffer against equity volatility

- Cash: Trailing 12-month returns of about 4%, comfortably above inflation but lagging risk asset

Notably, every major category outperformed cash over the past year, with international developed and emerging markets taking the lead in January. Factors driving this outperformance include favorable currency movements against a softening U.S. dollar, improving economic data in key regions like Europe and Japan, and a rotation into value-oriented and cyclical sectors that had lagged previously. This broadening leadership—where smaller U.S. companies and foreign equities are gaining ground relative to the S&P 500—is a textbook characteristic of a maturing bull market. It helps reduces concentration risk and can offer

more pathways for returns, rewarding investors who avoid over-reliance on a handful of mega-cap names.

Looking Ahead: Risks for the Rest of 2026

The overall environment remains supportive, but we must acknowledge meaningful near-term risks, particularly those tied to politics.

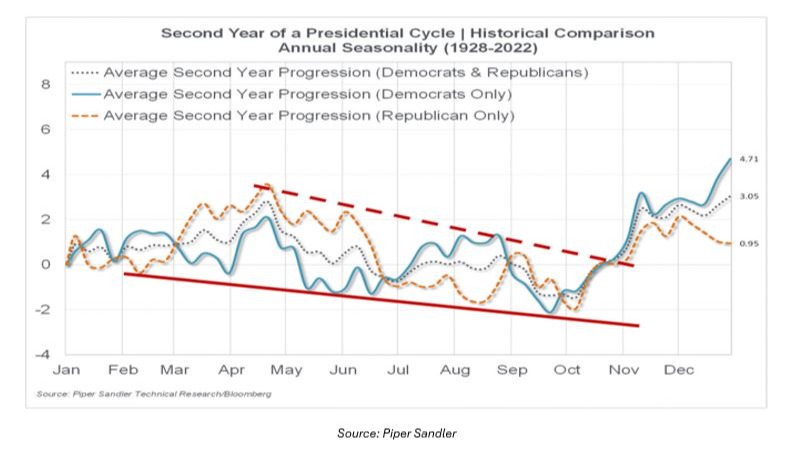

The primary headwind in 2026 is likely to be elevated volatility surrounding the November midterm elections—the second year of President Trump's term. Historical patterns across presidential cycles show that midterm years (the second year) tend to deliver below-average returns and higher choppiness compared to other phases. Data from sources like Ned Davis Research and various market analyses indicate that the S&P 500 has averaged lower performance in midterm years (often in the 4-6% range historically), with weakness frequently concentrated in the pre-election months due to campaign rhetoric, policy uncertainty, and debates over congressional control.

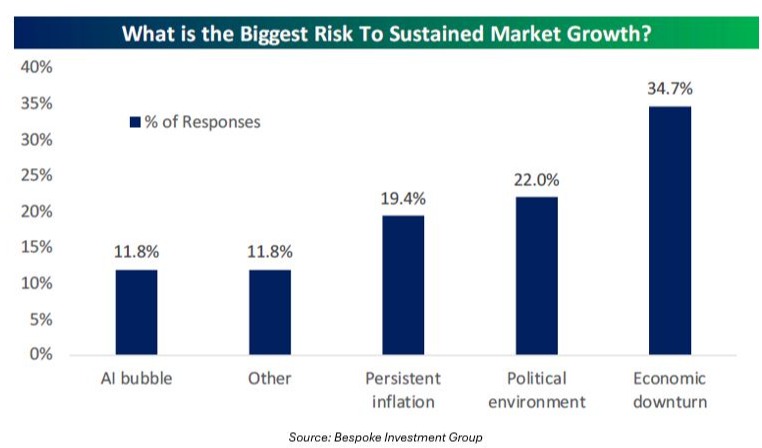

Investor sentiment surveys, including those from Bespoke Investment Group, frequently cite politics as a top concern—second only to recession fears, which currently appear low-probability given resilient economic indicators.

Markets can often trade at premiums entering these periods, which can amplify short-term pressure. That said, history also shows that much of the uncertainty resolves after the votes are counted, especially in scenarios with divided government that limit extreme policy shifts.

Our guidance remains straightforward: Maintain discipline. Avoid reactive moves driven by headlines or short-term noise. Volatility is an inherent part of markets—and when rooted in temporary factors like elections, it often creates attractive entry points for long-term investors rather than permanent damage.

Tailwinds Supporting the Bull Market

Fortunately, powerful counterbalancing forces are in play to support continued progress.

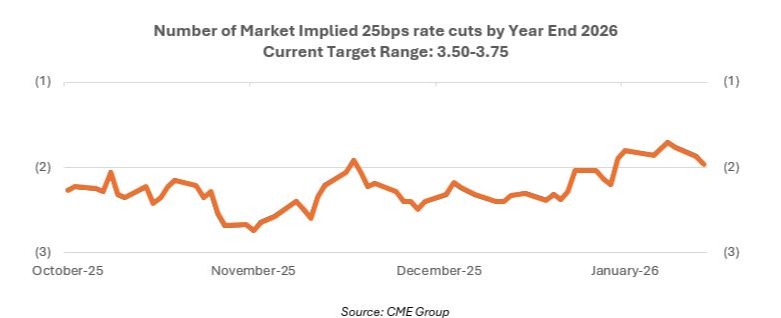

First, Federal Reserve policy continues to lean accommodative. Market expectations (and our base case) point to roughly two additional rate cuts in 2026, gradually guiding the fed funds rate toward ~3%. This follows measured easing initiated in 2025 and aligns with a backdrop of stable inflation and a softening but still-healthy labor market. The transition to a new Fed Chair (Kevin Warsh) in mid-2026 is unlikely to disrupt this trajectory significantly.

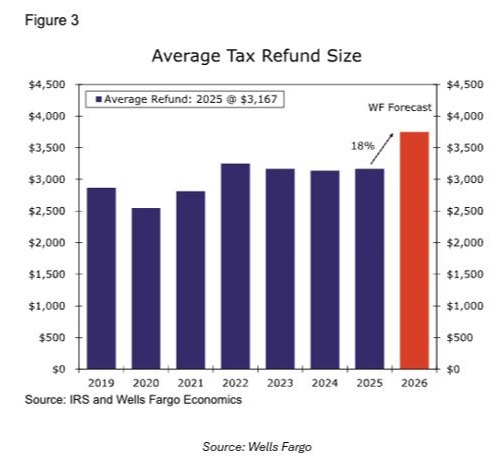

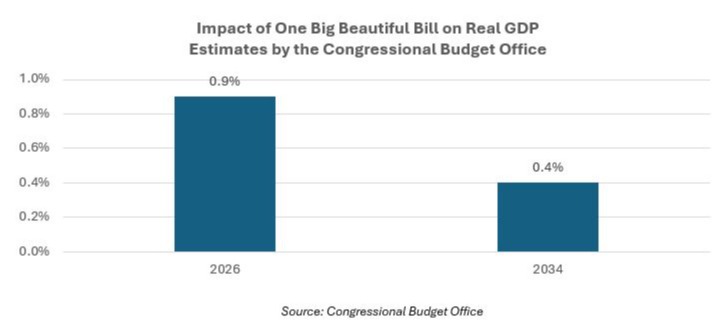

Second, fiscal stimulus from the One Big Beautiful Bill Act—enacted in 2025—continues to deliver front-loaded economic boosts in 2026. Key elements include meaningfully higher tax refunds (Wells Fargo estimates up to 18% higher on average), reduced payroll withholding for increased take-home pay, and enhanced consumer spending capacity.

The Congressional Budget Office projects this package could add approximately 1% to GDP growth in 2026, with lingering positive effects in subsequent years. Combined with ongoing monetary support, these dynamics provide a favorable setup for corporate earnings expansion, business investment, and overall economic resilience.

Bottom Line: Constructive Outlook

January's broad-based rally sets a promising tone for the year. While midterm-related chop is probable in the months ahead, the underlying fundamentals—earnings momentum, policy tailwinds, and the advantages of diversification—tilt the balance toward continued bull market advancement. We stay committed to long-term principles: focusing on quality growth, global exposure, and disciplined rebalancing rather than attempting to time political events.

If this evolving landscape raises questions about your personal plan—whether it's retirement timing, risk tolerance, or portfolio adjustments—please don't hesitate to reach out. Contact your RetirePath advisor by email, phone, or through our secure client portal. We're honored to serve as your steward, advocate, and confidant, helping you navigate 2026 with clarity and confidence.

* While diversification can help reduce market risk, it does not eliminate it. Diversification does not assure a profit or protect against loss in a declining market.

Index Benchmarks presented within this report may not reflect factors relevant for your portfolio or your unique risks, goals or investment objectives. Past performance of an index is not an indication or guarantee of future results. It is not possible to invest directly in an index.

The S&P 500® Index, or the Standard & Poor's 500® Index, is a market-capitalization-weighted index of the 500 largest U.S. publicly traded companies.

The MSCI ACWI (Morgan Stanley Capital International All Country World Index) Ex-U.S.® Index is a stock market index comprising of non-U.S. stocks from 22 developed markets and 24 emerging markets.

The Bloomberg Aggregate Bond® Index broadly tracks the performance of the U.S. investment-grade bond market. The index is composed of investment-grade government and corporate bonds.

The Russell 2500™ Index measures the performance of the small to midcap

segment of the US equity universe, commonly referred to as "smid" cap. The Russell 2500 Index is a subset of the Russell 3000® Index. It includes approximately 2500 of the smallest securities based on a combination of their market cap and current index membership.

The Congressional Budget Office (CBO) is a federal agency within the legislative branch of the United States government that provides budget and economic information to Congress.

Gross domestic product (GDP) is the total monetary or market value of all the finished goods and services produced within a country’s borders in a specific time period. As a broad measure of overall domestic production, it functions as a comprehensive scorecard of a given country’s economic health.

This communication may include forward looking statements. Specific forward-looking statements can be identified by the fact that they do not relate strictly to historical or current facts and include, without limitation, words such as “may,” “will,” “expects,” “believes,” “anticipates,” “plans,” “estimates,” “projects,” “targets,” “forecasts,” “seeks,” “could’” or the negative of such terms or other variations on such terms or comparable terminology. These statements are not guarantees of future performance and involve risks, uncertainties, assumptions and other factors that are difficult to predict and that could cause actual results to differ materially.