As your financial partners, we wanted to take a moment to share why we manage your portfolio the way we do—especially when markets get bumpy, or headlines feel loud. Our process is built to help you reach your goals, like a secure retirement. Here’s a simple look at why we do what we do, backed by some smart research we lean on.

Why We Mix Stocks, Bonds, and Cash

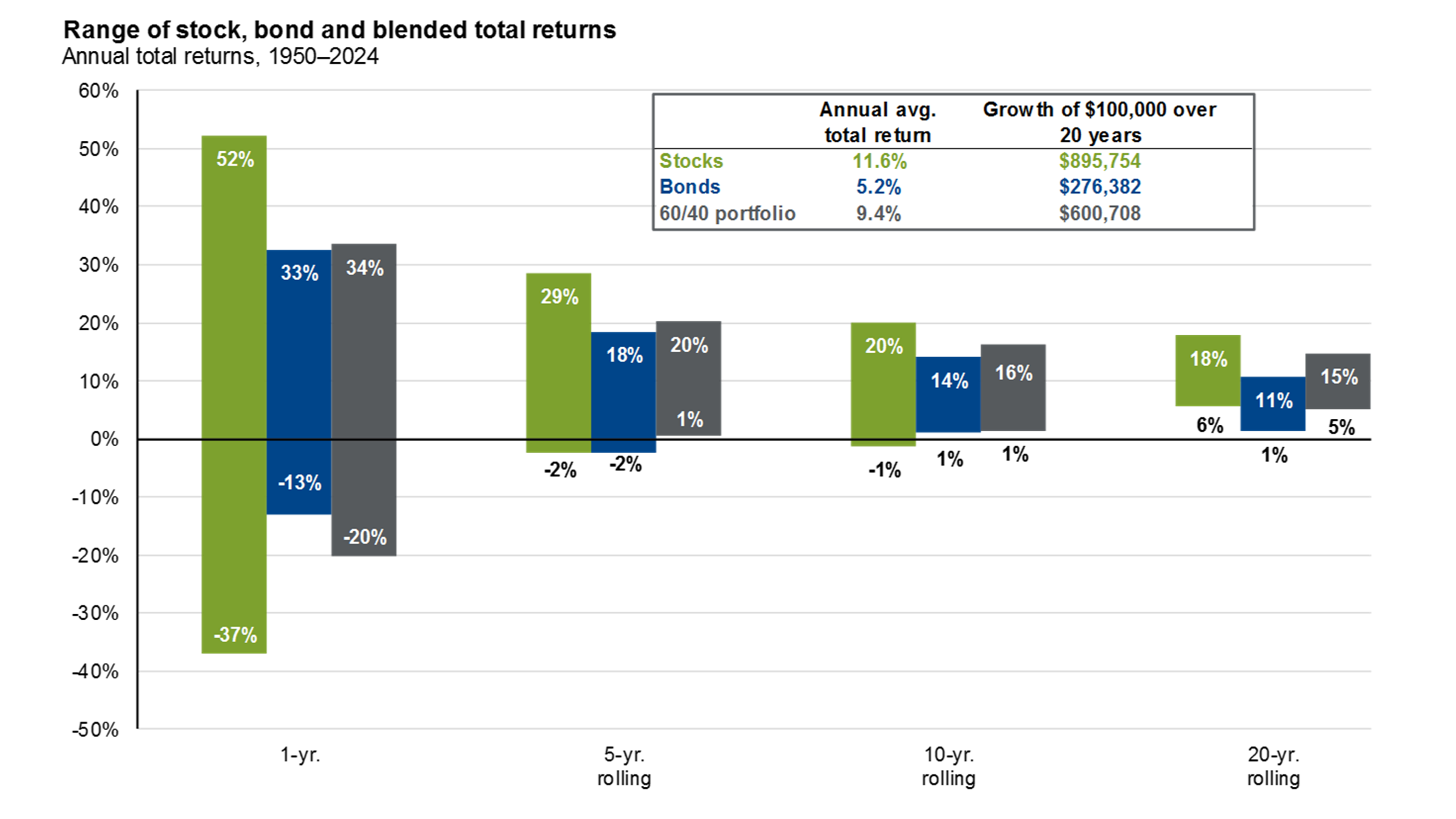

When you're in retirement your portfolio isn’t all in one basket—it’s a blend of stocks, bonds, and cash. Why? Because each plays a different role. Stocks aim for growth, bonds bring some calm when markets dip, and cash keeps money handy for emergencies. Research from experts like Roger Ibbotson (in a study called "The Importance of Asset Allocation" from the CFA Institute) shows this mix can explain over 90% of how your portfolio performs over time. In plain terms, it’s like having a team where everyone has a job—together, they smooth out the ups and downs so you can stay on track. Want to dig deeper? Check out a visual below of how these asset classes mix together over time.

Source: Bloomberg, FactSet, Federal Reserve, Standard & Poor’s, Strategas/Ibbotson, J.P. Morgan Asset Management.

Returns shown are based on calendar year returns from 1950 to 2024. Bonds represent Strategas/Ibbotson for periods prior to 1976 and the Bloomberg Aggregate thereafter. Growth of $100,000 is based on annual average total returns from 1950 to 2024. Past performance is no guarantee of future results.

Guide to the Markets – U.S. Data are as of March 31, 2025.

Why We are Long-Term Investors with a Portion in Stocks

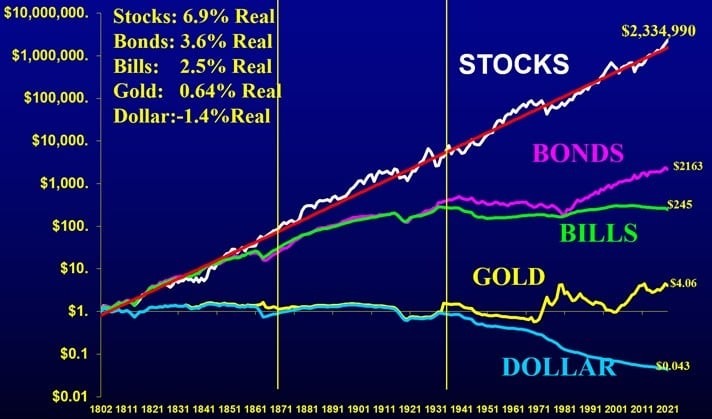

You might wonder why we put any money in stocks if they can be a rollercoaster. The answer is growth. Generally, stocks have the greatest potential to keep pace with or exceed inflation and growing your savings for the future—like retirement trips or helping your family. A professor named Jeremy Siegel studied this for years (in his book "Stocks for the Long Run") and found stocks have historically grown about 6.9% a year after inflation, way more than bonds or cash. Yes, there’s risk, but we believe it is worth it for the potential reward over time. We match that risk to what you’re comfortable with. Curious? You can see more below with research (Source: Jeremy Sigel).

Source: Siegel, Jeremy, Stocks for the Long Run (2014), With Updates to 2023. Past Performance is not indicative of future results. Stocks: The total returns after inflation on the broadest index of stocks available at the time. (Stocks-real-total return index: 1802-2022). Bonds: the total returns on an index on U.S. government bonds after inflation. (Bonds-real-total return index: 1802-2022. Bills (total returns on U.S. Treasury Bills after inflation. (Bills-real-accumulative index: 1802-2022). Gold: The value of $1 of gold bullion after inflation. (Gold-real-price index: 1802-2022). Dollar: The purchasing power of one U.S. dollar. (Money: 1802-2022). Index performance assumes reinvestment of dividends, but does not reflect any management fees, transaction costs or other expenses that would be incurred by a portfolio or fund, or brokerage commissions on transactions in fund shares.

Why we at RetirePath Advisors believe a Financial Plan Integrating Goals-Based Wealth Management Can Support a Successful Retirement

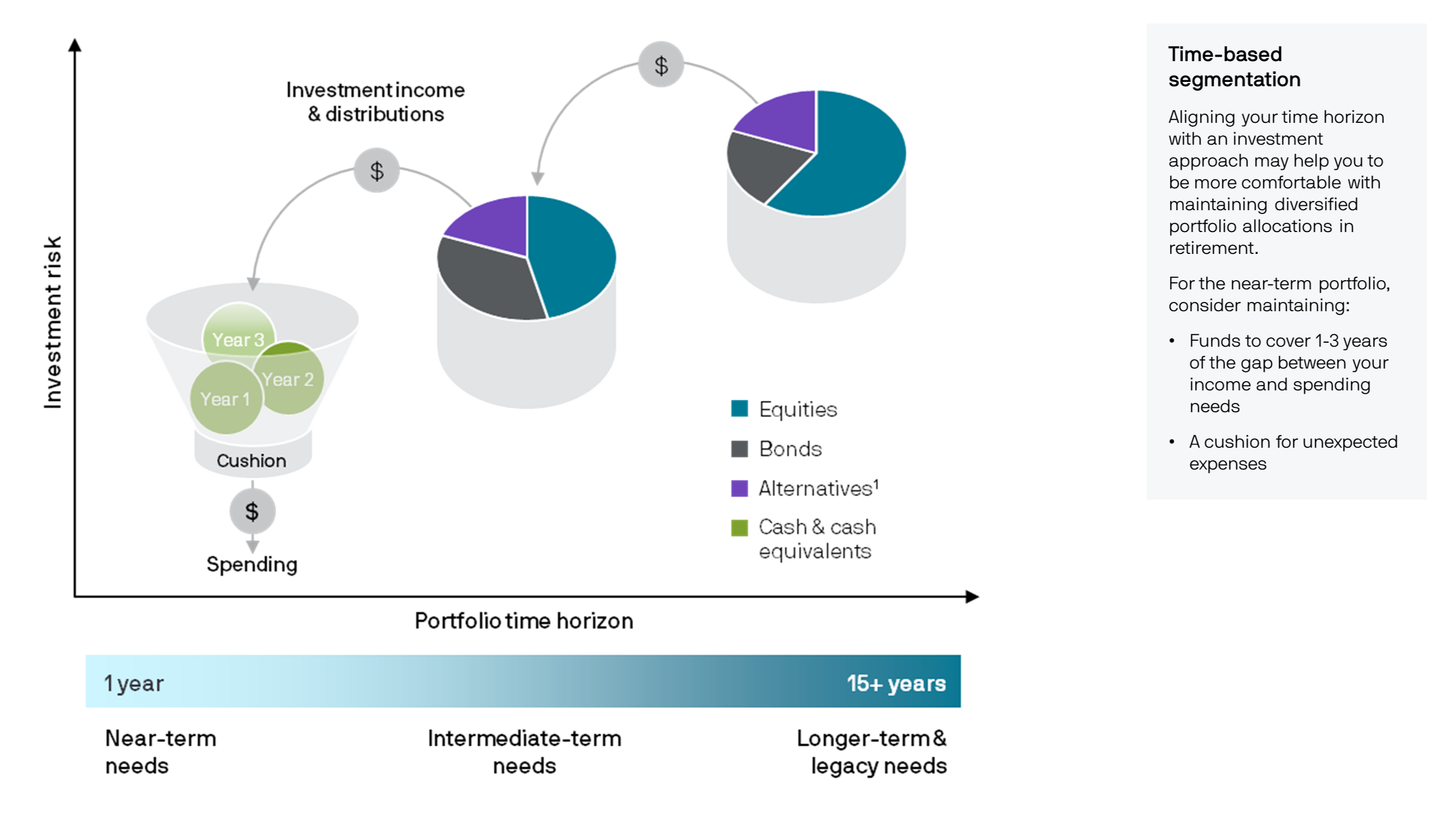

The focus of your financial plan isn’t just picking investments—it’s having a plan that fits your life. Whether it’s retiring comfortably or leaving a legacy, we tie your portfolio to those dreams. Research from the Financial Planning Association (in a 2014 study by Dave Yeske and Elissa Buie) shows people with plans feel more confident and save better. They’re also more likely to stick with their strategy when markets wobble, instead of panicking. A plan lets us adjust as things change, keeping you steady. See a visual below on how this may be implemented in retirement.

Source: J.P. Morgan Asset Management.

Source: For illustrative purposes only. Bonds are subject to interest rate risks. Bond prices generally fall when interest rates rise. The price of equity securities may rise or fall because of changes in the broad market or changes in a company’s financial condition, sometimes rapidly or unpredictably. Equity securities are subject to stock market risk, meaning that stock prices in general may decline over short or extended periods of time. Investing in alternative assets involves higher risks than traditional investments and is suitable only for the long term. They are not tax efficient and have higher fees than traditional investments. They may also be highly leveraged and engage in speculative investment techniques, which can magnify the potential for investment loss or gain.

1Equity, fixed income and cash are considered traditional asset classes. The term “alternative” describes all non-traditional asset classes. They include private and public equity, venture capital, hedge funds, real estate, commodities, distressed debt and more. J.P. Morgan Asset Management.

We’re here to make this work for you—balancing growth, safety, and a clear path forward. If you’d like to talk about your plan or just chat, please reach out to your RetirePath advisor.