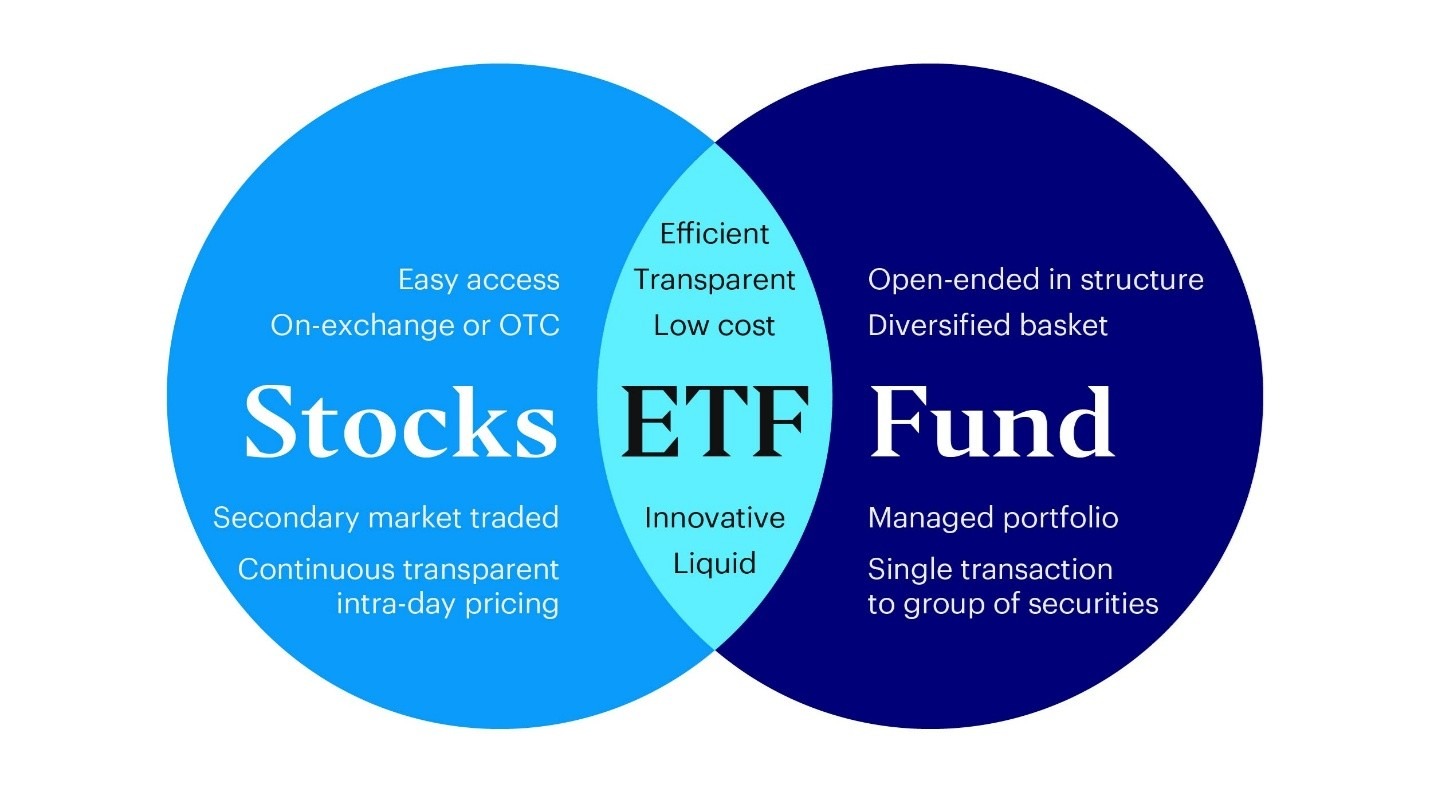

Exchange-traded funds changed the investing world when they first appeared in the early 1990s. The first U.S. ETF launched in 1993. It opened the door to a new way of buying into the market. These funds combined two good features. They offered diversification like mutual funds. But they traded like stocks throughout the day.

Source: Invesco

The Rise of ETF Popularity

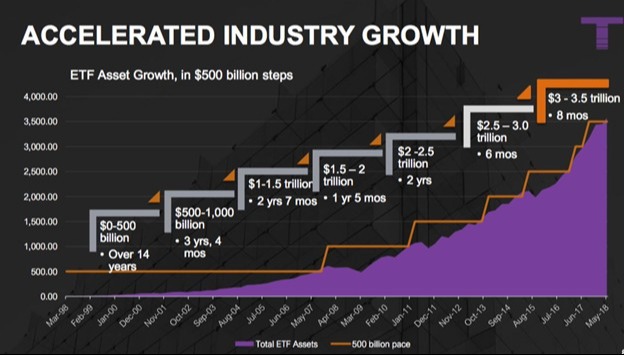

ETFs grew rapidly over the past three decades. In 1993, there was just one fund. Today, there are over 3,600 ETFs in the United States. Global assets in ETFs now exceed $10 trillion.

Source: Investment Company Institute (ICI), 2024. As of December 2023, there were 3,637 ETFs with $10.3 trillion in total net assets.

What may drive the popularity of ETFs?

- Lower costs - Most ETFs charge between 0.03% and 0.50% per year. Traditional actively managed mutual funds often charge between 0.50% and 1.50% per year.

- Tax advantages - ETFs use a special structure that can help reduce tax bills in many cases.

- Transparency - ETF providers show you exactly what the fund owns every day.

- Easy trading - You can buy and sell shares any time the market is open.

- Instant diversification - One share can give you exposure to hundreds or thousands of different investments.

Source: Fidelity and Morningstar, 2024. Average expense ratios: ETFs 0.48% (index) and 0.69% (active); mutual funds 0.60% (index) and 0.89% (active).

Source: The ETF Educator

A Universe of Asset Classes

Today, ETFs cover almost every type of investment: stocks (U.S. and international companies), bonds (government and corporate debt), commodities (gold, oil, agriculture), real estate (through REITs), alternative investments (digital currencies), and international markets (both developed and emerging). This wide range has made sophisticated investments accessible to individual investors.

Understanding Leveraged Single-Stock ETFs

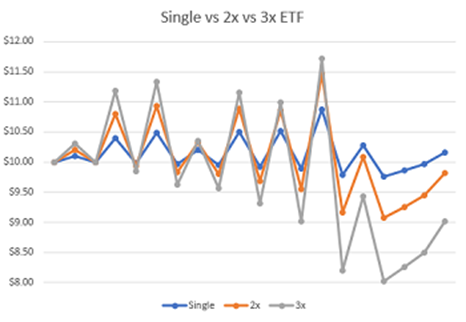

However, the ETF world has become much more complex. Some newer products carry serious risks. Leveraged single-stock ETFs are a prime example. These products amplify your exposure to a single company by two or three times.

Important Facts About Leveraged ETFs

Daily reset changes everything - These funds reset their leverage every single day. A 2x leveraged ETF won't simply give you double the return over a month or year. The math doesn't work that way.

Here's an example: A stock goes up 10% on Monday, then drops 10% on Tuesday. The stock ends roughly flat. But a 2x leveraged ETF tracking that stock actually loses money. This happens because of the daily reset feature.

You can lose more than you invest - The leveraged structure means losses get amplified too. In extreme cases, losses can exceed your original investment.

Complex instruments involved - These funds use derivatives (financial contracts like swaps and futures). They carry "counterparty risk," meaning the other party in the contract could fail to pay.

Built for day trading only - These products are designed for short-term trading. Holding them for weeks or months can produce unexpected results that differ dramatically from what investors expect.

Source: Study.com

The Emergence of Prediction Market ETFs

An even newer development may involve prediction market ETFs. I've noticed some recent ETF filings for these 'markets'. If approved, they may let you invest in the outcomes of future events like elections, Federal Reserve decisions, or corporate mergers, all inside your brokerage account.

Key Concerns

Win-or-lose propositions - Regular stocks go up and down gradually. Prediction markets involve yes-or-no questions. You either win or lose completely.

Different way of analyzing - When you invest in stocks, you look at company earnings. Prediction markets are pure speculation on events. There are no earnings reports to study.

Unclear regulations - The rules governing these products are still being developed. That creates uncertainty and risk.

Hard to fit into a portfolio - How do you decide how much to invest in election outcomes versus stocks and bonds? These questions don't have clear answers yet.

The Role of a Financial Advisor with Fiduciary Responsibilities

These changes show why we believe working with the right financial advisor matters more than ever. As ETFs have become more complex, investors face more difficult decisions.

A financial advisor with fiduciary responsibilities has a legal duty to put your interests first. Fiduciaries must recommend what's truly best for you. That's a higher bar. They typically charge fees based on your account size rather than earning commissions. This removes a major conflict of interest.

How An Advisor Supports You

- Product screening - They identify which ETFs might work for you and spot products that don't fit your needs.

- Risk identification - They understand leverage, derivatives, and tracking errors. They explain these risks in plain language.

- Portfolio balance - Their goal is to ensure your investments match your goals and help prevent inappropriate risks.

- Expert navigation - As products get more sophisticated, professional knowledge becomes more valuable.

Summary

The ETF industry has changed dramatically since 1993. It has brought many investment strategies to regular people. But today's landscape includes concerning developments: products with two- or three-times leverage, funds that profit when stocks fall, single-company bets with amplified risk, and potentially speculation on event outcomes.

Easier access now comes with increased complexity. Products once limited to sophisticated institutional investors are now available to anyone with a brokerage account.

If you invest in ETFs, consider these points: Balance your investment portfolio that includes ETFs with lower-risk core holdings such as broad-based index ETFs and diversified bond funds. Read the fund prospectus and understand how it works. Question complex products that require extensive explanation. Consider working with a financial advisor with fiduciary responsibilities. Recognize that different ETFs carry very different risk levels.

An advisor can help you tell the difference and evaluate which products, if any, make sense for your specific situation, goals, and comfort with risk.

Important Disclosures

This material is provided for informational purposes only and is not solely intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The views and strategies described may not be suitable for all investors. They also do not include all fees or expenses that may be incurred by investing in specific products. Past performance is no guarantee of future results. Investments will fluctuate and when redeemed may be worth more or less than when originally invested. You cannot invest directly in an index. The opinions expressed are subject to change as subsequent conditions vary. Advisory services offered through Thrivent Advisor Network, LLC.